No business can survive without a list of rules and regulations. To maintain this compliance, businesses have to follow the rules and regulations that are related to their industry. Businesses consider “maintaining compliance” a challenge as the rules are always changing. If you fail to stay up to date on these compliance rules, it can damage your company’s reputation.

What is Compliance Management?

Compliance management is the process of monitoring and assessing an organization’s internal systems to make sure that they comply with industry regulations.

Maintaining compliance isn’t just the role of top management, it comes down to everyone within the organization. The knowledge and understanding should correlate with the organization’s goals. All employees should be aware of how they can follow compliance standards. This helps in smooth working operations.

Importance of Compliance Management

As technology is becoming a major part of all sectors of our lives, legal regulations are becoming fiercer. Compliance management is crucial for every business as non-compliance can lead to legal and financial penalties, data theft, and damage to a business’s reputation.

Compliance management software or verification software can help financial institutions to keep up with compliance requirements.

Here are all the reasons why businesses need to comply with industry rules and regulations:

- Avoid Violations

Noncompliance with industry rules and regulations can hurt your business’s financial health. According to a recent study, it came to light that businesses without a compliance management system were imposed fines 2.71 times more than organizations with a system in place.

These fines amounted to $14.83 million annually. The same report also stated that the annual cost for compliance management is $5.47 million. Businesses operating in financial industries especially need to comply with industry standards and regulations.

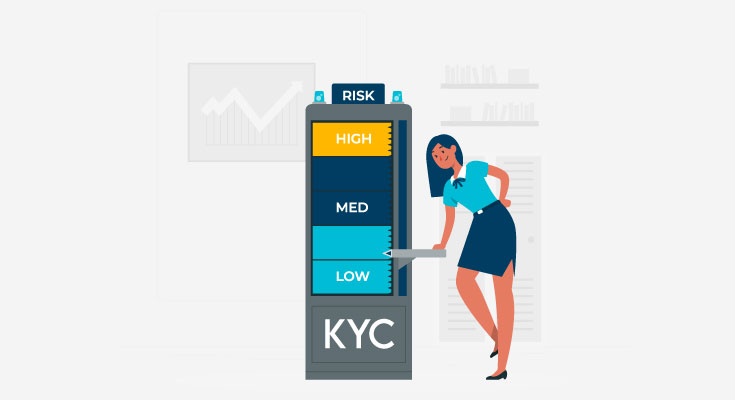

- Helps in Evaluate Security Risks

Complying with rules and regulations allows businesses to evaluate and manage security risks. Not just written guidelines and documents, but organizations need proper systems that can help to maintain compliance.

Risk assessments help evaluate the level of risk an organization faces at any given time and uncover potential risks. In addition to continuous monitoring, compliance management tools like KYC verification software can help fix vulnerable parts of operations.

- Protect Against Data Breaches

In case you fail to follow compliance requirements, it can lead to data breaches, and legal penalties, and it can hurt your business’s reputation. Every year, the number of data breaches is increasing, leading to the loss of millions of dollars worth of data. That’s not all. These data breaches ultimately increase the number of ID theft cases, leading to a whole new domino chain of fraud.

Challenges of Compliance Management

The reason why businesses shy away from compliance management is the challenges they face. Complying with laws and maintaining them throughout the organization is a major task.

- Regular Changes in Laws

Regulatory bodies often keep changing the rules and regulations based on current fraud trends. As new cyber threats move quickly across industries, regulatory bodies have to make immediate changes to rules to help organizations protect customers.

- Large Enterprises with A Lot of Employees

Managing and maintaining compliance is most challenging for larger enterprises. With a large workforce, it can be tough to make sure everyone is following the compliance initiatives. This leads to complex organization systems and can increase the risk of data breaches.

- Scattered Working Environments

As organizations now have both on-site and remote workforces, it becomes even more challenging to get an accurate view of compliance status. As a result, it has been challenging for most organizations to manage and monitor for risks and weak points.

Compliance Management Best Practices

Compliance management is a major process that requires a multi-faceted approach. You need to build a system that allows you to monitor all environments at the same time. Here are some best practices that you can follow for compliance management.

- Conduct Policy Audits

If your organization’s policy was written years ago, then most likely it needs to be added. Go through your organization’s compliance management policy, and take note of all the things that look dated. An audit will reveal gaps and weak points in your policy. Try to fix all the issues and you’ll be able to come up with a newer and stricter compliance management policy.

- Train Your Staff

Your staff needs to have a complete understanding of how they can maintain compliance throughout the organization. If your staff are your weakest link, then just making policies won’t solve anything.

Training helps reinforce policies and procedures and helps you handle employee questions and concerns. You should also schedule training sessions throughout the year to make sure all the employees are up to date on compliance standards.

- Continuous Monitoring and Due Diligence are the Keys

Data security and privacy legislation are some industry standards that want organizations to manage their cybersecurity standings. While privacy and security are two completely different things, they do go hand-in-hand.

The new privacy laws require businesses to consider “privacy by design” or “security by design,” and the use of continuous monitoring solutions. Businesses need to note that they should perform due diligence on third-party vendors. They can do this by using vendor bank account verification solutions.